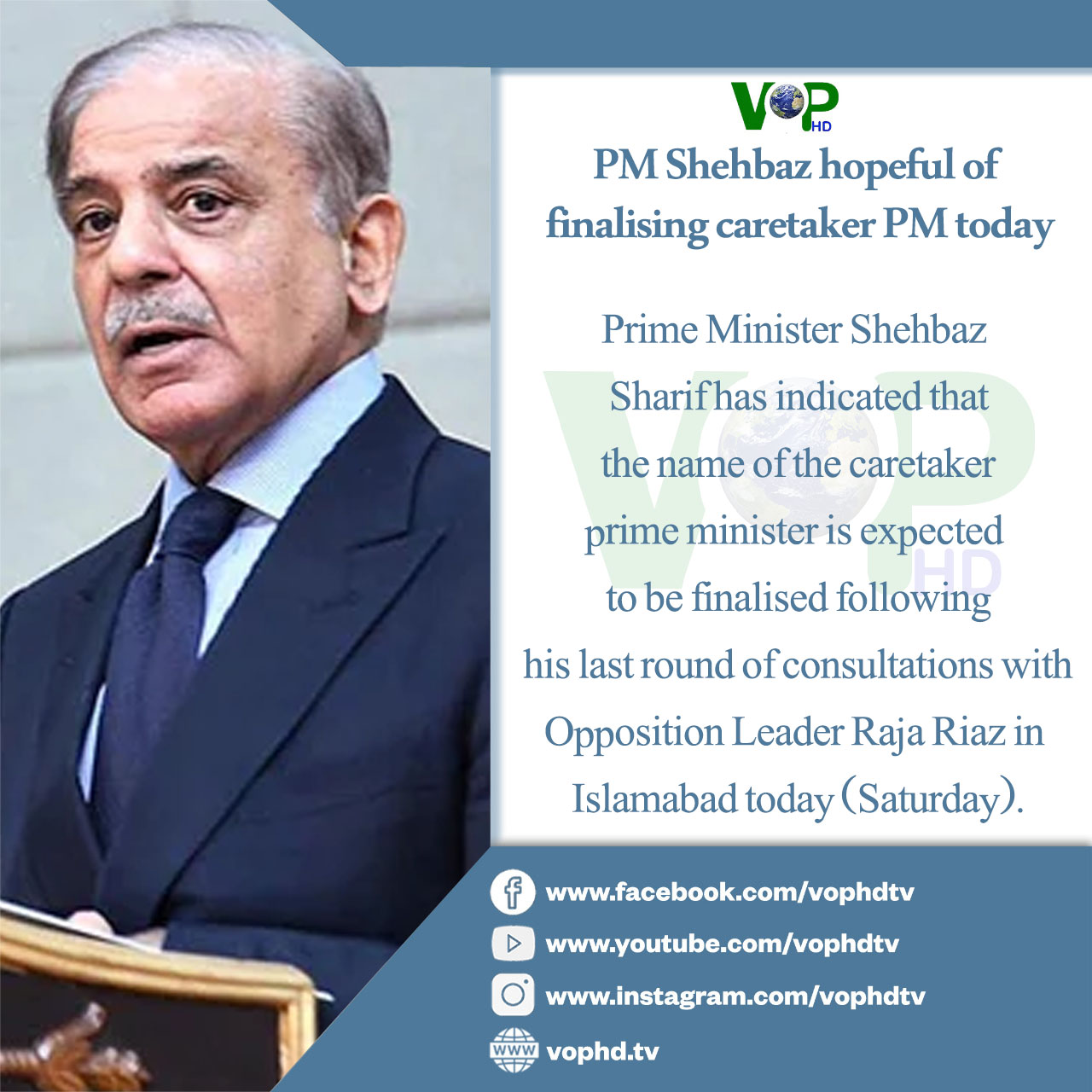

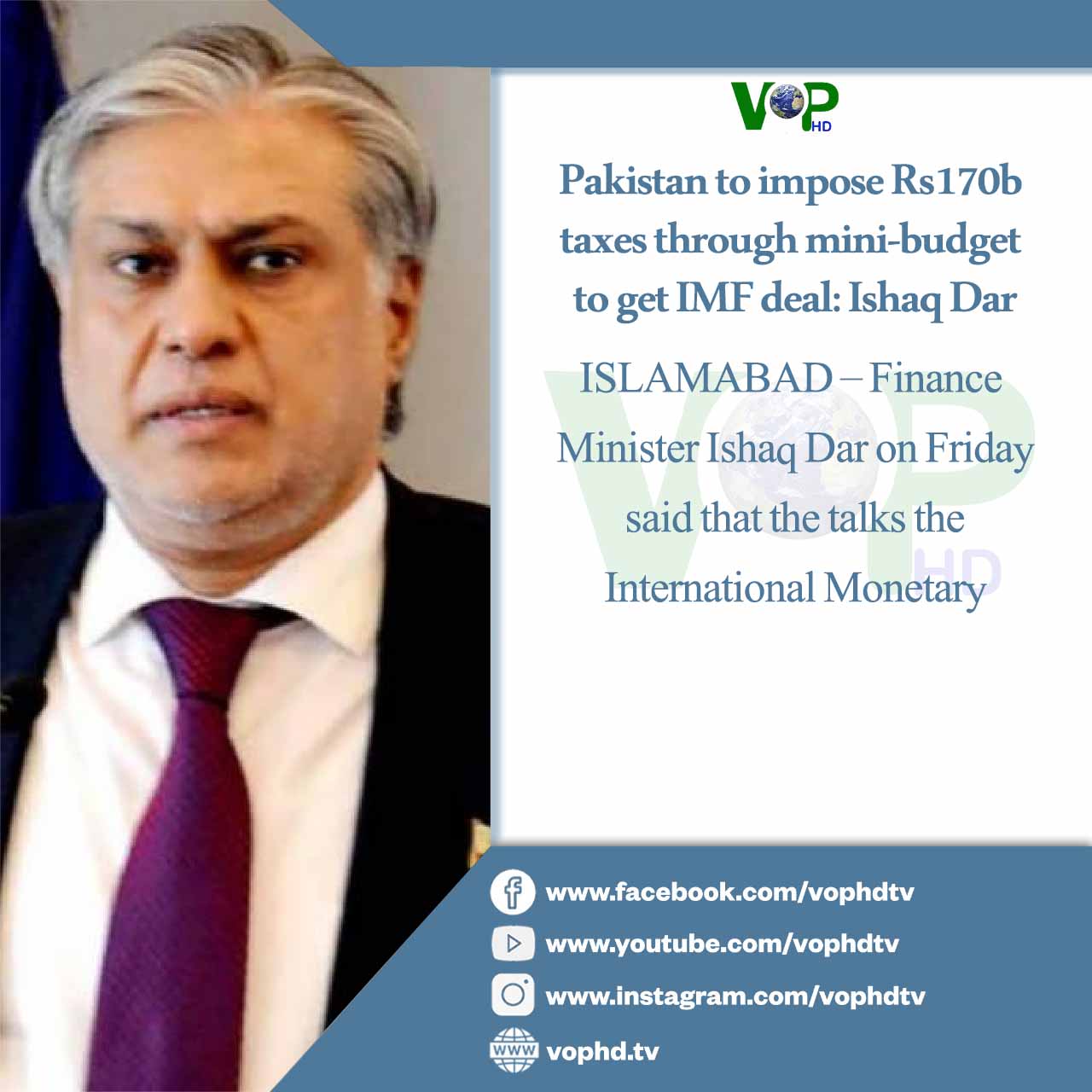

Interim govt jacks up petroleum prices to historic high

ISLAMABAD: The caretaker government has increased prices of petroleum products by up to Rs20 per litre for the next fortnight amid a rise in global oil rates — the highest in the country’s history.

“Petroleum prices in the international market have increased during the last fortnight. As a result the consumer prices in Pakistan are also being revised,” the Finance Division said in a statement late Tuesday.

The petrol has been increased by Rs17.50 per litre while high speed diesel (HSD) hiked by Rs20 per litre.

The new fuel prices are effective from August 16.

| Product | Existing price w.e.f Aug 1 | New price w.e.f Aug 16 | Change |

| Petrol | 272.95 | 290.45 | +17.50 |

| Diesel | 273.40 | 293.40 | +20 |

Earlier on August 1, the former Pakistan Democratic Movement (PDM)-led government had announced a massive Rs19 per litre increase in the price of petrol and diesel, which it said was done amid rising global oil prices

The announcement was due on July 31, but the government did not issue new rates as the officials tried to maintain or reduce the rates — keeping in view the impact of the price hike on inflation-weary people.

Ishaq Dar, who made the announcement as the finance minister for the last time as his government’s dissolved on August 12, said the increase was inevitable as Pakistan had agreed with the IMF on slapping petroleum development levy (PDL) to the rates.

The latest fuel price hike is likely to trigger a fresh wave of inflation in August.

Inflation hit a record 38% in May but the State Bank of Pakistan (SBP) decided to keep the key interest rate unchanged at 22% amid nominal decline in inflation last month.

The Monetary Policy Committee (MPC) particularly noted that year-on-year inflation is likely to remain on a downward path over the next 12 months, which implies a significant level of positive real interest rate.

Years of financial mismanagement have pushed Pakistan´s economy to the limit, exacerbated by the COVID-19 pandemic, a global energy crisis and record floods that submerged a third of the country last year.

But Islamabad struck a $3 billion standby deal with the International Monetary Fund (IMF) last month that could provide temporary relief for the country´s ballooning foreign debt.

The deal forces the government to scrap a range of subsidies that help the poor but the fuel price hike is largely in line with a rise in oil globally.